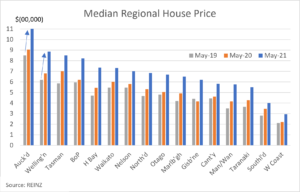

Earlier this week the Real Estate Institute of New Zealand released house price data for May reporting the familiar and increasingly concerning theme that house prices continue to rise. The Auckland region hit a new record house price again, of $1.148 million. Auckland City, North Shore City, Manukau City, Rodney District and Waitakere City all now have median prices above $1million, with only two Districts, Papakura ($900,000) and Franklin ($822,000), sitting below $1 million.

While this is not a race we necessarily wanted to join, Wellington City is hot on Auckland’s heels recording a median house price of $1.057 million in May.

At a national level, annual house price inflation of 32.3% lifted the national median price to $820,000, from $620,000 in May 2020. While the median price wasn’t a new record, it was the highest annual percentage increase since records began.

Wendy Alexander, Acting Chief Executive at REINZ, observed that a lack of total housing supply is continuing to push up house prices, with total inventory sitting at its second lowest level. This appears to be delaying either the impact of the Government’s March 23 housing announcements or the normal winter slowdown.

At a regional level, Median house prices in the Wellington region increased 30.3% year-on-year to $885,000 in May 2021. Mirroring the increase in the median price there has been a sharp increase in the number of properties selling for $1million or more. Last May 10.9% of properties in the Wellington region sold for $1million or more, in May this year the figure was 36.8% which in-turn compares to 61.8% for the Auckland market.

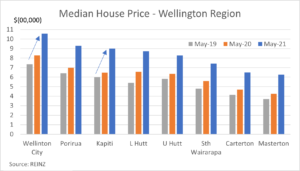

As noted previously, the median price in Wellington City was $1.057 million recording a 27.3% increase over the year. Porirua City is also edging towards the $1 million mark, recording a median price of $930,000 following a 33.0% lift over the year.

In the Hutt Valley, Lower Hutt experienced a 33.2% annual increase in the median house price to a record $873,500, while Upper Hutt recorded a 30.4% annual increase to $828,000.

In recent months, we have witnessed a trend of people looking to the surrounding districts for opportunities to find more reasonably priced property, particularly given the opportunities to work from home presented by our experience with lockdowns in 2020. Reflecting this, price growth has been strong in both Kapiti and the Wairarapa, with prices up sharply over the year:

- Kapiti recorded a 39.0% increase in the median price to $900,000

- South Wairarapa recorded a 32.6% increase in the median price to $742,555

- The Carterton District reported annual house price growth of 38.3% to $650,000

- Median house prices in the Masterton District increased by a whopping 47.1% over the year to $625,000.

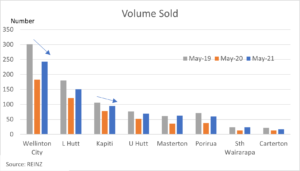

Wellington is the region with the lowest inventory levels, at just 5 weeks. This is half the level in Auckland which has 10 weeks of inventory. This in turn continues to constrain sales growth. The REINZ had the following observations for the region:

- Listings were down -14.2% from April 2021, contributing to the -20.8% decrease in inventory for the region – leaving 746 properties available for prospective purchasers, or 5 weeks of stock

- Investor activity has started to ease slightly, which may show some impact over the coming months in regard to sales volumes and inventory.

Questions continue to circulate over how sustainable the current trend is and the long-term impact it is having on a generation – and sectors of society – who are being left behind by rising property prices. For the present though, demand continues to be underpinned by low mortgage rates and the perceived need to snap-up the limited stock coming to market.

In early 2020, there were forecasts that house prices might fall as the COVID-19 pandemic took hold. The contrast with the present situation could not be starker. One of the main reasons’ economists were concerned that house prices might fall was the potential impact of the pandemic on the labour market. A spike in unemployment could in-turn have had severe repercussions for the property market. In the end, this largely did not come to pass with the unemployment peaking at 5.2% in September last year, well short of concerns that persistently lower economic activity might see unemployment reach levels around 9 to 12 per cent.

Likewise, looking forward it could take the likes of a shock to the labour market to cause the type of disruption that will cause a drop in house prices. Absent a shock to the labour market (or some event), it is more likely that we will see house price growth settle lower, perhaps around 2-3% annually as foreshadowed by the Reserve Bank in their May Monetary Policy Statement. Time will tell, in the meantime forecasting the actual level they settle at is just short of pure guesswork.